6 Ways to Enjoy a Budget-Friendly Summer

It’s time for summer vacation, but you don’t want to lose sight of your budget completely. What do you do? Fortunately, we’ve got plenty of tips to help!

It’s time for summer vacation, but you don’t want to lose sight of your budget completely. What do you do? Fortunately, we’ve got plenty of tips to help!

SPRINGFIELD, Mo. – AGCU announced the recipients of our 2024 Scholarships, Thursday, May 2, during the Annual Business Meeting held at AGCU Operations Center.

Every year we award scholarships to a number of Youth Account Members who are graduating from high school and plan to attend an accredited college or university in the fall of their graduation year. It’s just our way of thanking our New Attitudes members who have chosen AGCU as their banking institution. If you would like to learn if you or a loved one qualify for an AGCU Scholarship, contact your local branch!

Meet This Year’s Recipients

Josiah Bonin

$3000 Scholarship

Josiah is graduating from Bonin Homeschool in Namur, Belgium, and plans to attend Southwestern Assemblies of God/Nelson University as a worship arts and jazz major. He is a member of the Conservatory of Namur Jazz Ensemble. Josiah has volunteered in community disaster relief efforts in both Verviers, Belgium, and Lake Charles, Louisiana. He serves on the worship team at his church and will be the worship leader at the upcoming AGWM Western Europe Youth Retreat.

Lauren Melton

$3000 Scholarship

Lauren is graduating from Hillcrest High School in Springfield, Missouri, and plans to attend Southeastern University as a finance major. She is salutatorian of her class, president of National Honor Society, and student body president. Lauren is also a member of her school’s Fellowship of Christian Athletes and Future Business Leaders of America, and she has qualified for FBLA state. Additionally, she serves on the youth leadership and worship teams at her church.

Truman Griessel

$3000 Scholarship

Truman is graduating from Ozark High School in Ozark, Missouri, and plans to attend Lindenwood University as a communications major with an emphasis in sports broadcasting and media production. He is a member of National Honor Society, DECA, Fellowship of Christian Athletes, as well as Ozark High School’s marching band, jazz band, and wind symphony. Truman serves in the children’s program at his church.

Elyse Rogers

$3000 Scholarship

Elyse is graduating from Classical Conversations Educational Homeschool Cooperative in Springfield, Missouri, and plans to attend Harding University as a pre-medicine/biochemistry major. She is student government treasurer and captain of her speech and debate team. Elyse serves in the children’s ministry at her church, as well as a member of her church choir. She has participated in and won awards in numerous speech and debate tournaments.

James Letterman

$3000 Scholarship

James is graduating from Glendale High School in Springfield, Missouri, and plans to attend Evangel University and study pre-dentistry. He has been on the cross country and track teams throughout his high school career and has obtained leadership positions on the teams. James has been part of the Royal Ranger program at his church for most of his life and earned the Gold Medal of Achievement. He has also participated in various community and church volunteer projects.

Alexander Worthley

$1000 Scholarship

Merrell K. Cooper Memorial Scholarship

Alexander is graduating from Nixa High School in Nixa, Missouri, and plans to attend Evangel University as a pre-medical biology major. He is a member of the National Honor Society and Mu Alpha Theta – Mathematics Honor Society. Alexander is on his school’s cross country and track teams and participates in Fellowship of Christian Athletes. He has earned the Gold Medal of Achievement with Honors in Royal Rangers and serves on the youth worship team at his church.

Much more than a catchphrase, our tagline is our passion, our reason why we do what we do. This is the impact of your membership with AGCU. Learn More About Banking with a Purpose

The more you use AGCU for your day-to-day banking needs, the more you help support worthy causes – both locally and worldwide. We donate 10% of our annual earnings to support churches and ministries, educational scholarships and programs, and humanitarian efforts. Every day, we provide financial services to people across the United States and missionaries in 190 countries around the world.

In 2023, together, we donated a total of $379,035

When you’re trying to save and manage your money, it can be tough to decide the right account to use. Savings accounts are ideal for funds you want to put away for emergency or special purposes, while checking accounts are the way to go for money you’ll spend. But what if you’re looking for something that will help you save with the flexibility to spend?

When you’re trying to save and manage your money, it can be tough to decide the right account to use. Savings accounts are ideal for funds you want to put away for emergency or special purposes, while checking accounts are the way to go for money you’ll spend. But what if you’re looking for something that will help you save with the flexibility to spend?

Look no further than a money market savings account. These are perfect for funds you don’t need immediate access to but may need to withdraw from in the future. Typically, you’ll earn a higher return without the risk of the stock market or the restrictions of a CD.

One of the most attractive features of money market savings accounts is how your funds are “liquid” — they don’t have a maturity date or term requirements. This means you can access money in your account anytime, usually without penalty*

The level of security combined with the ease of accessibility can be ideal if you have occasional, large expenses such as tuition payments, household repairs, or even unexpected medical fess. You’ll simply earn your dividend while waiting for a need to spend.

Premier Money Market accounts offer flexibility in how you access funds. In fact, you can make deposits, Write Checks, make withdrawals, and transfer funds into your checking account, so you’re free to use your money in a pinch without any major effort at all!

Whatever purpose you have for your money — whether saving or spending — a money market savings account is an ideal place to keep your funds.

Money market savings accounts offer a rate of return that surpasses your typical savings account. In most cases, the more money you keep in your account, the higher your interest rate is. This is especially beneficial in a rising-rate environment when rates are expected to increase — giving your money the best chance to grow!

Our Premier Money Market Account takes this concept to the next level with a tiered system designed to reward your commitment to saving.

Minimum Balance |

Rate |

APY |

| $50,000-$74,999 | 3.50% | 3.56% |

| $75,000-$99,999 | 3.75% | 3.82% |

| $100,000 + | 4.00% | 4.07% |

Funds in your Money Market account are insured by the NCUA up to $250,000. This means you can keep a large sum of money in your account without the risk of losing it to a market crash or a poor choice of investment. It’s a great opportunity to start saving with confidence!

AGCU shares your values and faith. We provide individuals, ministries, and businesses with the financial tools and knowledge they need to grow and thrive financially so they can transform our world through their generosity.

AGCU shares your values and faith. We provide individuals, ministries, and businesses with the financial tools and knowledge they need to grow and thrive financially so they can transform our world through their generosity.

The money you deposit in AGCU helps churches grow, ministries expand, businesses succeed, and individuals thrive. Whether it’s constructing or remodeling a new church building or funding a home loan, your money is working in the Assemblies of God community.

Click below to open a Premier Money Market Account or become a member of AGCU!

Speak face-to-face with an AGCU Video Banking Representative from anywhere.

Give it a try today! Video Banking Hours (CST): Mon – Fri: 9:00 a.m.- 5:00 p.m.

Apply through online application.

Do you have questions regarding becoming a member or opening an account? Call (417) 831-4398 or fill out our contact form and we will contact you!

At the Assemblies of God Credit Union, your membership actively supports ministry, education, and humanitarian causes. It’s more than just banking; it’s a faith-driven financial partnership we call Banking With A Purpose.

In the spirit of the holidays, let’s celebrate “12 Days of Impact” as we reflect on the incredible contributions your membership at AGCU makes to these and many more initiatives. Your membership truly matters, creating ripples of positive change that resonate far beyond the realms of traditional banking. As we step into the new year, let’s continue to make a difference together.

Convoy of Hope

Convoy of HopeA humanitarian, faith-based organization on a mission to feed the hungry and bring help and hope to communities in need. Through Disaster Services, Community Events, Agriculture, Women’s Empowerment, and Rural Initiatives, Convoy of Hope impacts lives globally, offering a helping hand where it’s needed the most.

Learn more about Convoy of Hope

Assemblies of God World Missions (AGWM) finds strength in your commitment to global missions. Your membership supports AGWM in reaching, planting, training, and serving worldwide. Together, we’ve seen countless lives transformed and churches planted, fulfilling the core values of the AG Fellowship. Every 54 seconds, someone comes to Christ, a testament to the impact your faith has globally.

Learn more about Assemblies of God World Missions (AGWM)

Your commitment to AGCU extends beyond borders, reaching communities within the United States through AG U.S. Missions. By supporting windows like Adult and Teen Challenge, Chaplaincy Ministries, and Intercultural Ministries, your membership becomes a beacon of hope, providing resources and encouragement where it’s needed most.

Learn more about Assemblies of God U.S. Missions

Education: Nurturing Minds, Building Futures

Education: Nurturing Minds, Building FuturesThrough AGCU, you’ve empowered educational initiatives, contributing to dozens of colleges, universities, public schools, and private Christian education. Your commitment to scholarship programs, educational materials, and financial education reflects a dedication to nurturing minds and shaping future leaders.

Project Rescue

Project RescueYour membership takes a stand against human trafficking through support for Project Rescue. This multinational network fights to restore hope to survivors, and your involvement makes a significant impact in the ongoing battle against this global scourge.

Learn more about Project Rescue

YiPoA – Youth in Pursuit of Awakening

YiPoA – Youth in Pursuit of AwakeningYour commitment to the Youth in Pursuit of Awakening (YiPoA) movement is a testament to your dedication to raising a generation that loves Jesus and lives out the gospel. Through events and programs, you’re actively participating in shaping future leaders who will impact the Kingdom.

Learn more about Youth in Pursuit of Awakening (YiPoA)

Fellowship of Christian Athletes

Fellowship of Christian AthletesWith your membership, Fellowship of Christian Athletes (FCA) has the power to use the platform of sport to reach coaches and athletes with the transforming power of Jesus Christ. Your commitment to integrity, serving, teamwork, and excellence resonates through FCA’s mission to lead every coach and athlete into a growing relationship with Jesus Christ.

Learn more about Fellowship of Christian Athletes (FCA)

REVFresh

REVFreshYour benevolence through REVFresh refreshes ministry leaders, addressing personal needs and encouraging generous living. Your partnership supports a culture of support and care, reflecting the values of integrity, accountability, responsibility, and dedication.

Learn more about REVFresh

Springfield Giants

Springfield GiantsYour support of Springfield Giants Inc. signifies your commitment to character development through competition. The attributes of a Giant—character, accountability, responsibility, and dedication—are instilled in the youth, shaping them into confident future leaders.

Learn more about Springfield Giants

Simply Loved Orphan Care

Simply Loved Orphan CareThrough Simply Loved Orphan Care, your membership contributes to projects and funding for orphanages in Eastern Europe. Your support ensures better care and preparation for life after the orphanage, reflecting your commitment to making a difference in the lives of these children.

Learn more about Simply Loved Orphan Care

Light The Way Ministry

Light The Way MinistryYour membership supports Light The Way Ministry, spreading the light and hope of Jesus Christ beyond the church walls. Through gatherings, events, and year-round efforts, your involvement becomes a source of transformation, bringing healings, deliverances, baptisms, salvations, and breakthroughs.

Learn more about Light The Way Ministry

The Young Entrepreneurs Showcase

The Young Entrepreneurs ShowcaseYour commitment to the Young Entrepreneurs Showcase provides a platform for young people to showcase their talents and entrepreneurial spirit. Through your support, you’re actively nurturing young minds and fostering a culture of innovation.

Learn more about Young Entrepreneurs Showcase

Much more than a catchphrase, our tagline is our passion, our reason why we do what we do. This is the impact of your membership with AGCU. Learn More About Banking with a Purpose

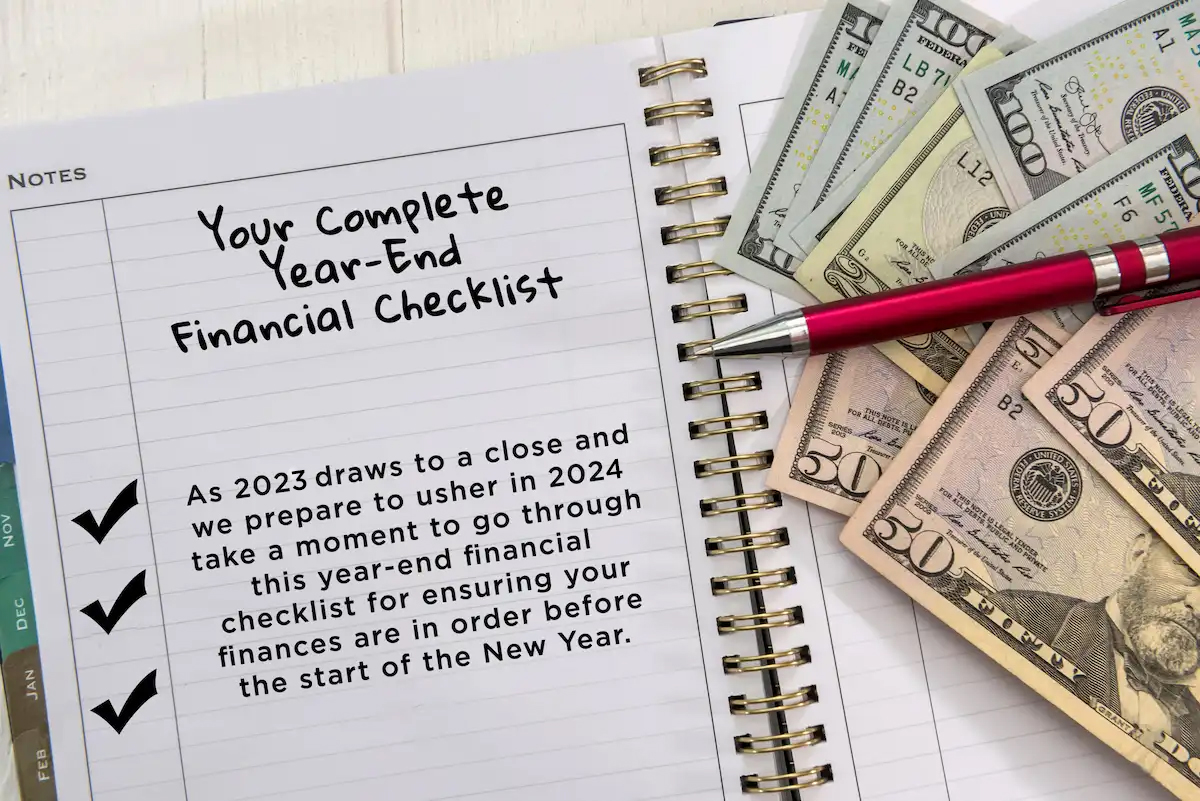

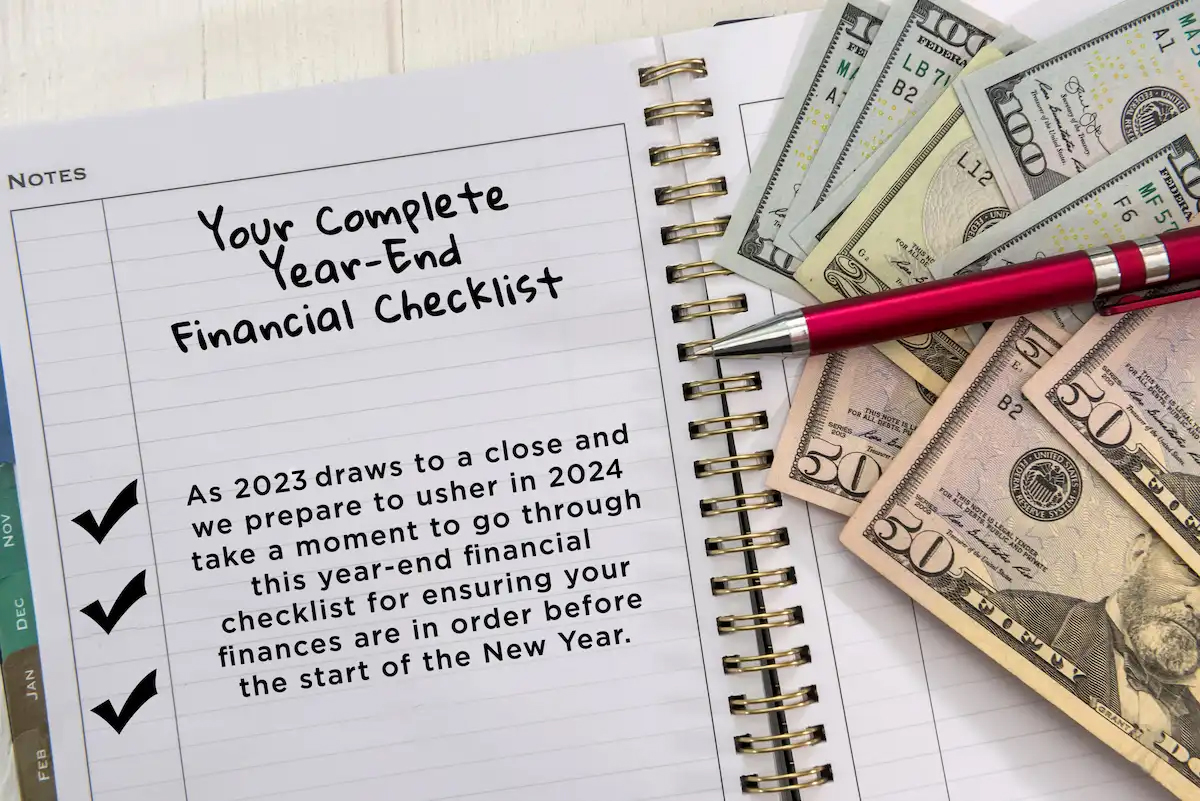

Is your monthly budget still working well for you? Are you stretching some spending categories or finishing each month in the red? Take some time to review your budget and make any necessary changes.

If you have a 401(k), check to see that you are taking full advantage of your employer’s matching contributions. If you haven’t contributed as much as you can, you have until the end of the year (Dec. 31, 2021) to catch up; to a limit of $19,5001. If you turned 50 this year, you are eligible for an additional catch-up contribution of $6,5001. If you anticipate getting a holiday bonus, consider putting this money toward your debt.

Likewise, if you have an IRA, you have until April 15 to scrape together the maximum contribution of $6,000, with an additional $1,000 if you are age 50 years or older.1

Give your debt an annual checkup by reviewing your outstanding debts from one year ago and holding up the amounts against what you now owe. Have you shed debt from one year ago, or is your debt growing? If you haven’t made any progress, or your debt has grown, consider taking bigger steps toward paying it down in 2022, such as consolidating your debt with a personal loan.

The end of the year is a great time for an annual credit checkup. It’s a good idea to review your statements each month to check for fraudulent charges, but you can also request a free copy of your credit report from all three credit agencies once a year. Get your free annual credit reports here, and take a close look at each report. Look for accurate, updated information and any errors, like charges you don’t remember making, or other signs of possible identity theft. If you find any wrongful charges, be sure to dispute them immediately.

Take some time at year’s end to rebalance your portfolio and to see if your asset allocation is still serving you well. You may need to make some changes to your mix of stocks, bonds, cash and other investments to better reflect the current state of the market.

Has your family situation changed in the past year? If it has, be sure to switch the beneficiaries on your accounts and life insurance policies to accommodate these changes.

The end of the year coincides with open enrollment for health insurance policies. This is your chance to select the employer benefits you want for the coming year. If you miss this window, you will be stuck with the benefits you chose last year or with no benefits at all.

It’s a good idea to review your W-4 annually and see if the amount of tax being withheld from each paycheck needs to be adjusted. If you’re not a numbers person, ask your accountant or tax advisor for help. Changing up the numbers just a bit can make a significant difference in your tax bill at the end of the year. Or, if you usually get a large refund, adjusting the amount withheld can mean enjoying a larger paycheck throughout the year instead of giving the government an interest-free loan to be paid back in one lump sum at year’s end.

Much more than a catchphrase, our tagline is our passion, our reason why we do what we do. This is the impact of your membership with AGCU. Learn More About Banking with a Purpose

1. Based on amounts provided by IRS.gov.

Member Length |

Minimum Deposit |

Term |

*APR |

*APY |

| 0-9 Years | $2,500.00 | 12 Months | 4.95% | 5.06% |

| 10-19 Years | $2,500.00 | 12 Months | 5.10% | 5.22% |

| 20+ Years | $2,500.00 | 12 Months | 5.35% | 5.48% |

Open an AGCU Certificate of Deposit and lock in a fixed interest rate so you can enjoy the peace of mind of a guaranteed interest rate on the money you save.

By choosing the Loyalty CD, you not only secure competitive rates but also benefit from the stability and reliability of AGCU. We’re committed to your financial well-being, and this exclusive offering is one of the ways we express our appreciation.

Your Rates Deserve a Raise! Invest in AGCU’s Loyalty CD and watch your CD earnings grow. At AGCU, we value your loyalty and strive to provide you with the best financial solutions. Start maximizing your money’s potential with our Loyalty CD today.

Scammers are using the AGCU phone numbers to make calls. The caller claims to be with AGCU and is asking for personal and confidential information. AGCU’s phone number may show up on the caller ID, but the call is actually from a scammer, not AGCU. If you receive a call and the person asks for confidential information, hang up!

NEVER give out confidential information, such as account numbers, social security numbers, mother’s maiden name, or passwords to an unsolicited caller!

If you get a phone call, email, or a text message from AGCU or your credit card company, or anyone asking you to do something, pick up the phone and call AGCU’s Member Care team. Don’t call back to the number that sent you the text!

Learn more about spotting scams

AGCU Member Care services are just a call or click away. We’re proud to serve you and our community.

Call:

417-831-4398 or 866-508-AGCU (2428)

Monday-Friday 7:30 am- 5:00 pm CT

Top 5 Reasons to Choose AGCU

Top 5 Reasons to Choose AGCUChoosing your financial institution is an important decision. Banking with a Purpose means your faith is always in action. Your financial choices actively support missions, ministries, and humanitarian causes. It’s more than banking; it’s a faith-driven financial partnership. Here are the top five reasons to consider banking with AGCU:

Competitive Rates on Your Deposits

Competitive Rates on Your DepositsAGCU doesn’t just provide loans and savings accounts; we’re the folks that want your money to grow while you sleep. If you’re all about making your money pull double duty as it works hard for you AND the Kingdom, we’re right there with you. We’ve got checking accounts that can earn you as much as 2.5% APY, Jaw-dropping CD rates, and Money Market accounts that offer both flexibility of access and high earnings.

We’re All in This Together

We’re All in This TogetherAGCU shares your values and is committed to serving the Assemblies of God Church. But here’s the best part: when you bank with us, you’re not just managing your money; you’re part of something bigger. We donate a 10% of our earnings, like a tithe, to support ministries, humanitarian causes, and education. You’re not just banking; you’re investing in a faith-driven mission every time you choose AGCU.

We Get You

We Get YouFinancial alignment is essential, right? We understand the unique culture, ministry, and dreams of the Assemblies of God community. We’re here to help you achieve your goals. We get the challenges you face and are here to support and secure your financial journey, no matter how tricky it gets.

Your Money, Your Way

Your Money, Your WayAGCU’s reach goes far and wide. As a member, you’re not confined to local branches. You have access to the extensive Shared Credit Union CO-OP network of over 30,000 ATMs and 5,000+ shared branches nationwide. That means more banking options and convenience wherever you go.

A Faithful Legacy

A Faithful LegacyAGCU has a rich history built on the call to serve its members. This legacy isn’t stuck in the past; it’s a living testament that will be felt for generations. We hold fast to Godly principles, ensuring that every member is part of a legacy rooted in faith and dedicated to serving the Assemblies of God community.

In a nutshell, AGCU – Assemblies of God Credit Union offers much more than just banking; it offers a faith-infused financial partnership with a purpose. It’s your money, your faith, and your values working together to create a better future for you and the world. Join us, and let’s make a difference, one deposit at a time.

Speak face-to-face with an AGCU Video Banking Representative from anywhere.

Give it a try today! Video Banking Hours (CST): Mon – Fri: 9:00 a.m.- 5:00 p.m.

Apply through online application.

Do you have questions regarding becoming a member or opening an account? Call (417) 831-4398 or fill out our contact form and we will contact you!

Much more than a catchphrase, our tagline is our passion, our reason why we do what we do. This is the impact of your membership with AGCU. Learn More About Banking with a Purpose

APY=Annual Percentage Yield

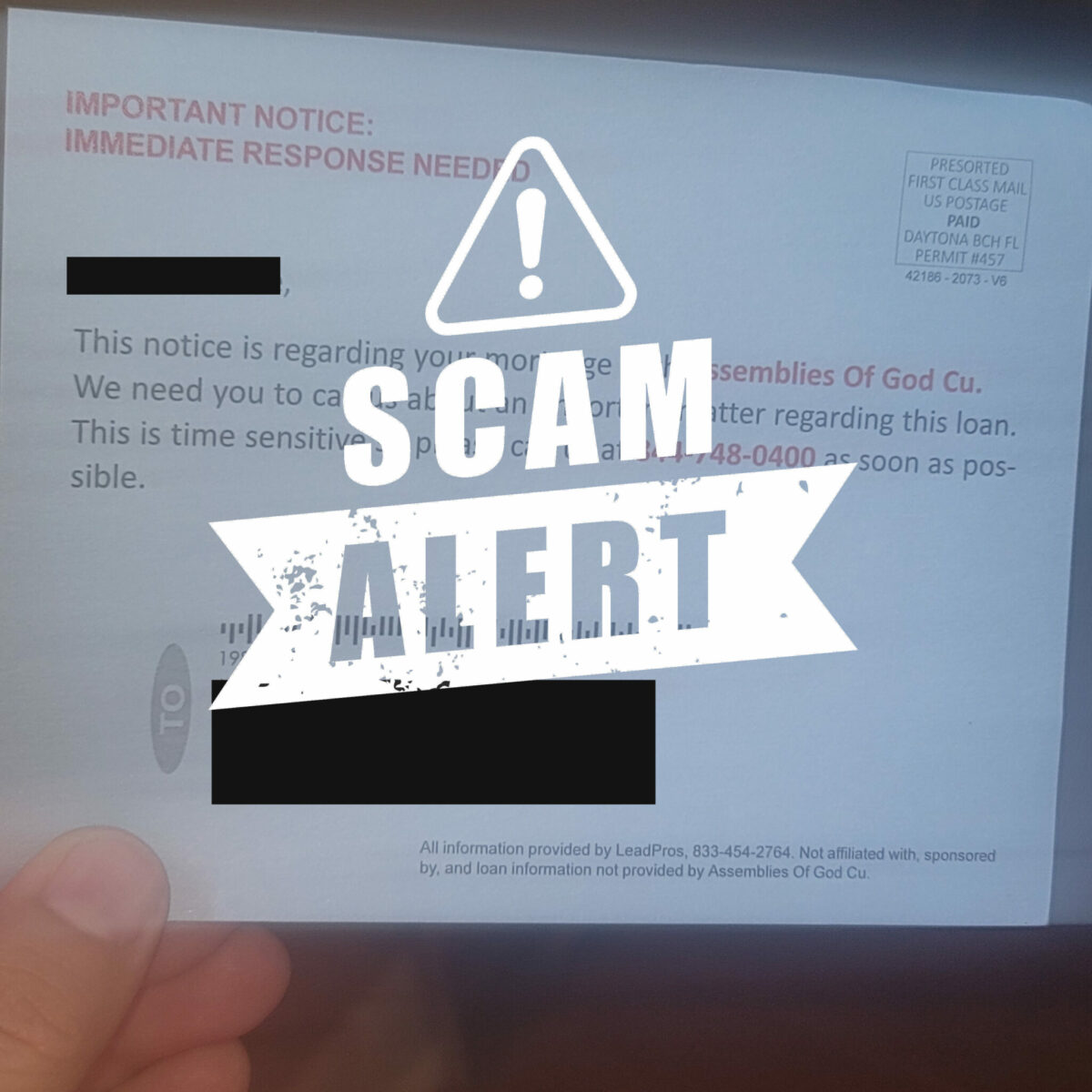

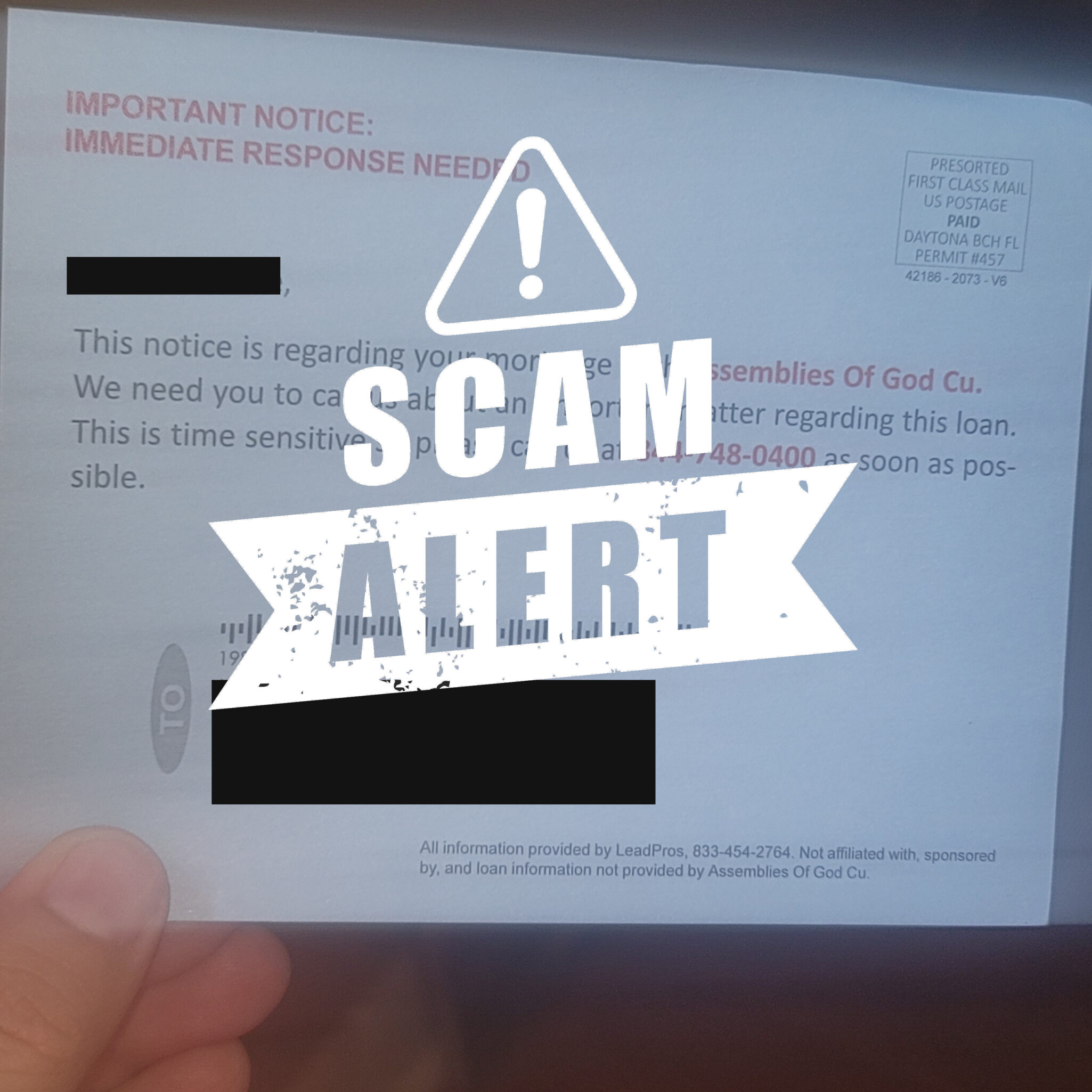

If you recently closed on a mortgage and have yet to receive a postcard in the mail requesting an “immediate response” to “an important matter” regarding your loan, just wait, It’s probably coming.

This is because a long-running mortgage scam that uses publicly available information such as a mortgage closing date to target new homeowners shows no signs of abating. How do we know? We recently got a little postcard ourselves.

These postcards (which come in a variety of colors) are being sent to consumers all around the country.

Please be aware that this is a scam and did not come from AGCU, or any financial institution. There is a small disclaimer in the bottom right corner indicating the sender is “not affiliated with, sponsored by, and loan information not provided by Assemblies of God Cu.” It further states that the information was provided by “LeadPros” Our research suggests this home warranty corporation is the culprit behind these postcards. The company has an “F” rating with the Better Business Bureau.

At AGCU, we’re committed to protecting our member’s personal information. We would never send you a postcard requesting that you call us regarding your mortgage. Likewise, we do not sell or otherwise distribute it to non-affiliated third parties.

However, some information about mortgages, regardless of what lender the consumer works with, is public record. That’s how someone like this may obtain your contact information. Do note that the account number listed does not match yours; this should immediately alert you to the likelihood of this being a scam.

We advise our members NOT to call the number listed. Calling the number may connect you with a real person, or it may connect you to automated recording prompts. Regardless, do not offer them your personal information.

The best thing to do is disregard the postcard. Dispose of it however you would any other junk mail you receive. In addition, please contact a Member Service Representative at 417-831-4398 should you have additional questions.

If you would like to take further action, consider filing a complaint with your State’s Attorney General’s Consumer Protection Division.

Dealing with debt can be overwhelming, and scammers are all too eager to exploit this vulnerability. Debt collection scams are on the rise, targeting individuals who are already stressed by their financial situation. Understanding how these scams work and knowing how to protect yourself is crucial. Let’s take a closer look at debt collection scams and how to avoid becoming a victim.

In a typical debt-collection scam, a fraudster poses as a debt collector and contacts the victim, insisting on immediate payment for an outstanding debt. They are often unrelenting, demanding a specific means of payment, such as a wire transfer or a prepaid debit card. However, the truth is that the caller is not a legitimate debt collector, and any money paid will go directly into their own pocket.

Recognizing the warning signs of a debt-collection scam is the first step in protecting yourself:

To safeguard yourself from falling victim to debt collection scams, follow these essential tips:

Dealing with debt is challenging enough without falling victim to scams. By following these guidelines, you can better protect yourself and your financial well-being from unscrupulous individuals seeking to exploit your financial troubles. Stay informed, stay vigilant, and ensure your financial future remains secure.

Please contact a Member Service Representative at 417-831-4398 should you have additional questions.

If you would like to take further action, consider filing a complaint with your State’s Attorney General’s Consumer Protection Division.

Much more than a catchphrase, our tagline is our passion, our reason why we do what we do. This is the impact of your membership with AGCU.

Learn More About Banking with a Purpose