What is a Credit Report?

Your credit report affects a dizzying array of things that go on in your life, so you really need to know what it is and what affects it. We’ve got the total breakdown!

Your credit report affects a dizzying array of things that go on in your life, so you really need to know what it is and what affects it. We’ve got the total breakdown!

Having your current address, phone number, and email on file ensures that you receive important notifications and updates about your account. It also helps prevent your account from becoming dormant and potentially classified as unclaimed property.

It’s time for summer vacation, but you don’t want to lose sight of your budget completely. What do you do? Fortunately, we’ve got plenty of tips to help!

You don’t need to have a pile of gold or a million dollars’ worth of jewelry to need a safe deposit box. Learn why you need one, what to put it in and how to handle the legal side!

Wire transfer scams can involve unexpected requests for money through email, phone call, or message. Scammers may pressure you to send money because it’s easy for them to take your money and disappear. Once the money is gone, it’s unlikely you’ll be able to get it back. Learn how to identify and protect yourself from these scammers

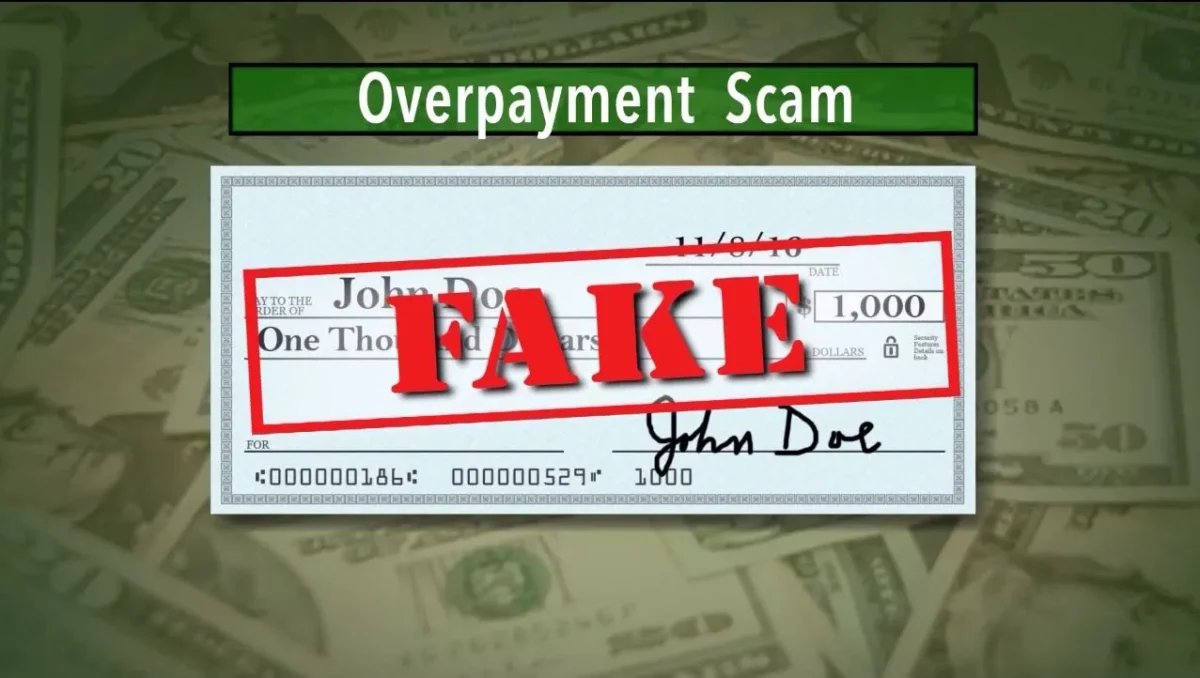

If you just got overpaid for an item you’re selling online, you may be caught in an overpayment scam.

At AGCU, we’re excited to introduce Finicity’s seamless integration with our digital banking platform, bringing you a revolutionary way to manage your finances. With Finicity, you can easily transfer money between your accounts at different financial institutions and get a real-time view of your financial health—all from the convenience of the AGCU dashboard.

Our money moves mostly via ACH and wire transfers, but there are some major differences between them, especially when it comes to speed and security. We’ve got it all explained!