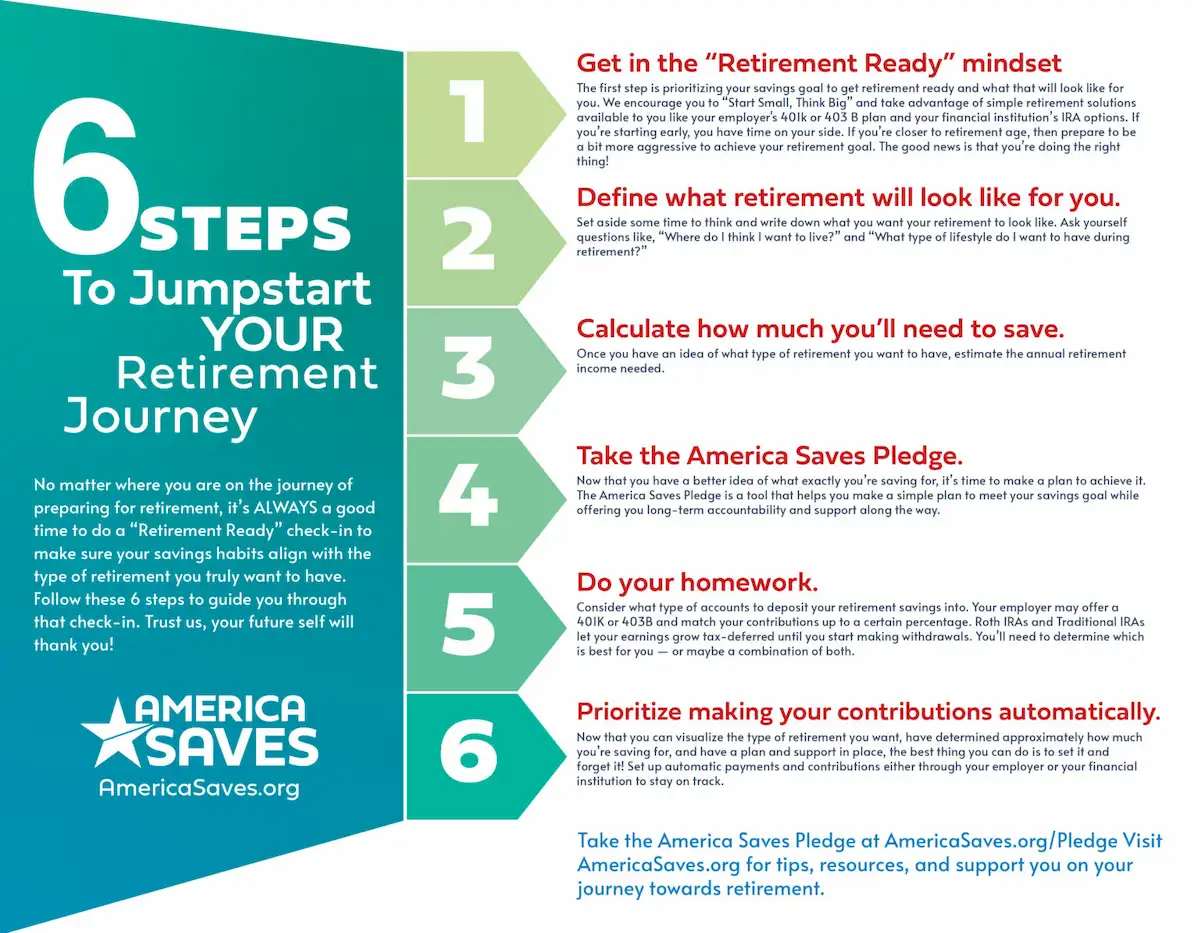

6 STEPS TO JUMPSTART YOUR RETIREMENT JOURNEY!

By Breanna Johnston, AFC® Candidate

Retirement is one of those endeavors that fall into the “someday” category. When living your day-to-day life as a person in their 20s, 30s, and even your 40s and those everyday expenses pop up, it’s more difficult to save for something that is seemingly so far away.

But as we all know — life comes at you fast. A 2020 survey by Charles Schwab of currently employed 401(k) plan participants found that saving enough for retirement continues to be a leading source of significant financial stress for all generations.

While studies show that 71 percent of Americans are adequately prepared for retirement, much of that includes receiving Social Security benefits under the current law. With Social Security payouts only scheduled to be paid at the full benefit amount through 2035, Millennials and Gen Z have to approach retirement from a different perspective — one that is diverse and doesn’t rely on Social Security benefits, if you can help it. The good news is that starting early allows you to reach your retirement goals more easily.

In today’s economy, we can’t overlook the fact that there are some people who are not making a fair living wage, making it difficult to save. But for those of us with the ability to save it’s important to understand that it’s never too late to start saving for retirement. Your future self will thank you!

So what are the steps to take when you’re ready to jumpstart your retirement journey? Glad you asked! Here are our six steps below.

1. GET IN THE “RETIREMENT READY” MINDSET.

The first step is getting in the right mindset, meaning-making your new savings goal a priority. We encourage you to “Start Small, Think Big” and take advantage of retirement solutions available to you like your employer’s 401K or 403 B plan or IRA options you can open on your own.

If you’re starting your retirement savings journey early, you have time on your side! However, if you’re closer to retirement age, then prepare to be a bit more aggressive in order to achieve your retirement goal. Research how to make catch-up contributions to your retirement savings, ultimately jump-starting a stalled plan.

The good news is this: it’s never too late! It is important to remember that saving anything is better than saving nothing. Even increasing your retirement savings by one percent can make a huge difference in the long run.

2. DEFINE WHAT RETIREMENT WILL LOOK LIKE FOR YOU.

Your retirement years will be as individual as you are! Have you visualized how you’d like your retirement to look and feel? Think about where you want to settle down. Will you stay put and have sweet tea and lemonade on the front porch most days or do you intend to travel far and wide? Most importantly, how much “annual income” will you need to achieve this envisioned lifestyle? Asking yourself these questions will help determine a rough estimate of how much to start saving now.

Someone who plans to travel and or have an active lifestyle when they retire may need to save more than someone who has a home that is paid off with no grand plans of world travel.

You will also need to consider exactly when you want to retire. This will help determine how much you should be saving annually. In the modern age, people pre-retire, half-retire or even never leave the workforce at all.

3. CALCULATE HOW MUCH YOU’LL NEED TO SAVE.

Once you have an idea of what type of retirement you want to have, estimate the annual retirement income needed. You want to ensure you are saving for the future you want. Most Americans are not putting enough money into their retirement fund every year in order to afford the life they want for themselves in the future.

What each person needs will vary widely based on a number of factors, including your current age, the age at which you plan to retire, if your partner or spouse has an income, your spending habits, and different sources of retirement income. There are also circumstances beyond your control, like how long you can expect to live based on family history.

While there is no hard and fast rule to determine how much to save by a specific age, many personal finance experts recommend having saved an amount equal to your annual salary by age 30, three times by age 40, and five times by age 50. While this can be overwhelming if you haven’t hit those milestones in your retirement savings yet, one small step you can take is to increase your contribution rate with each pay raise. Remember, building a savings habit and taking control of your finances, like you’re doing now, is worth celebrating.

4. TAKE THE AMERICA SAVES PLEDGE.

Now that you have a better idea of what exactly you’re saving for and how much, it’s time to consider how you’ll achieve your dream retirement. The America Saves Pledge is a tool that helps you make a simple plan to meet your savings goal while offering you long-term accountability and support along the way. Take the America Saves Pledge and visit AmericaSaves.org for tips, resources, and support on your journey towards retirement. Remember: savers who make a plan are twice as likely to save successfully!

5. DO YOUR HOMEWORK.

Consider what type of accounts to deposit your retirement savings into. Your employer may offer a retirement plan such as a 401K, 403B, or SEP-IRA and match your contributions up to a certain percentage. The most important consideration here is to take advantage of any employer benefits such as matching your contributions up to a certain percentage. Find out if your employer offers a match and contribute at least enough to maximize that benefit.

Individual Retirement Arrangements (IRAs) are also an option, and you can open one anytime through financial institutions or financial services providers. There are several different IRAs including the most common: Roth and Traditional. Roth IRAs can be withdrawn at anytime without penalty and are tax-free. Traditional IRAs may be tax-deductible and your earnings grow tax-deferred until you start making withdrawals. You’ll need to determine which is best for you — or maybe a combination of both. The IRS has put together a great comparison tool to understand the differences between the two accounts and decide which may be better for you.

6. PRIORITIZE MAKING YOUR CONTRIBUTIONS AUTOMATICALLY.

Now that you can visualize the type of retirement you want, have determined approximately how much you’re saving for, and have a plan and support in place, the best thing you can do is to set it and forget it! Set up automatic payments and contributions either through your employer or from a financial institution to stay on track.

The point of retirement savings is to keep it invested for the long term. This means avoiding dipping into your retirement fund for emergencies. Instead, create an emergency savings fund that you are also contributing to consistently.

Research by the Employee Benefit Research Institute shows that it typically takes 13 years or more of contributions to an account before you begin to reach a level of savings that is enough to fund a number of years of retirement as a supplement to Social Security. So don’t become discouraged if you feel you do not have enough savings in your retirement fund just yet.

Whatever path you choose to take toward retirement, the biggest step to take is being consistent. Retirement savings is a long-term commitment, but today’s work will pay off in the long run, literally. Take the America Saves Pledge and let us help you reach your goals, no matter what they are. Your future self will thank you!

Banking With A Purpose

Much more than a catchphrase, our tagline is our passion, our reason why we do what we do. This is the impact of your membership with AGCU. Learn More About Banking with a Purpose